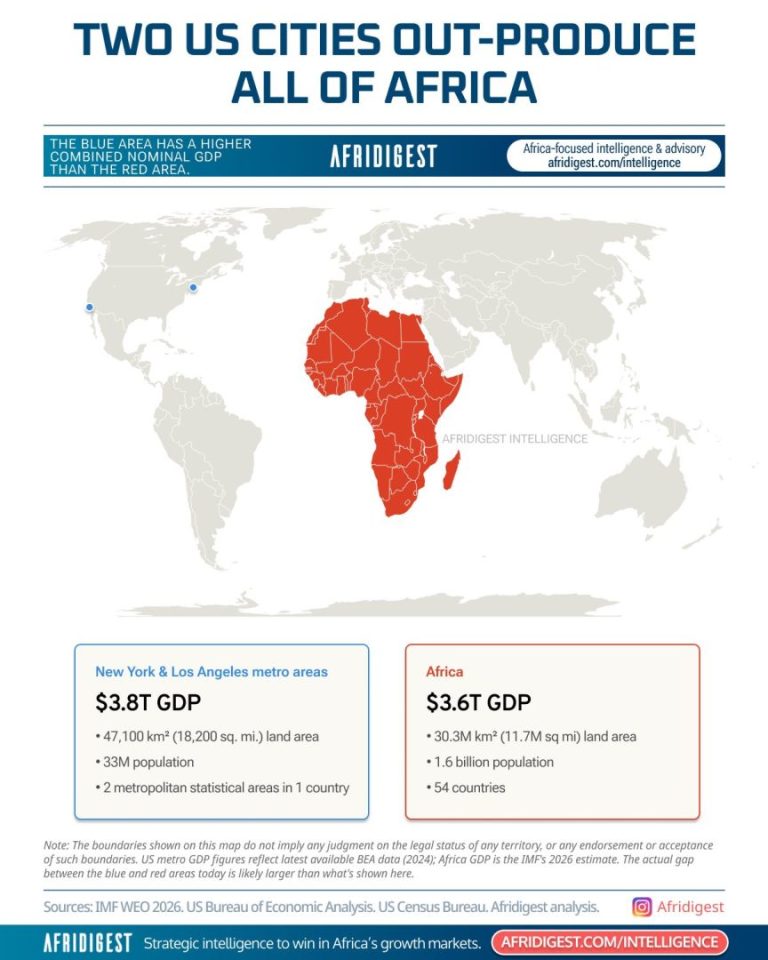

Two US metro areas produce as much as all of Africa.

New York and Los Angeles have a combined GDP of $3.8 trillion.

Africa — with its 54 countries, 1.6 billion people, and land area more than 3x the size of the US — has a GDP of $3.6 trillion.

That isn’t due to a lack of talent, ambition, or resources. Much of it is due to fragmentation.

New York and LA operate inside one currency, one regulatory system, and a single open market.

Africa contends with 40+ currencies, 50+ regulatory regimes, and significant cross-border frictions.

Consequently, in many cases across many African markets, it’s cheaper to trade with Europe, for example, than with the country next door.

The result is one of the world’s least integrated regional economies.

Intra-African trade accounts for less than 15% of Africa’s total trade, compared with roughly 60% inter-regional trade for Europe and Asia.

That’s why the idea of a more interconnected, low-friction, global Africa is so compelling. Integrate the market, and prosperity starts to compound.

Despite slow implementation, the AfCFTA remains a good overarching mechanism to reduce the frictions that exist.

But integration can’t be legislated from the top down alone.

It has to be built from the bottom up, too — with entrepreneurs, investors, and civic leaders helping to build the infrastructure and institutions that allow African markets to coordinate more effectively.

Ultimately, a more connected Africa won’t be magically conferred by the AfCFTA — it’ll have to be actively constructed.

GAIA — Global Africa Investment Alliance

Decision-makers across the continent and the world trust Afridigest for Africa-focused intelligence & advisory → Afridigest Intelligence

Sign up here to receive the Afridigest newsletter in your inbox.

Share: